Thames Water

Thames Water (TW) is in the news a lot at the moment so I thought I would offer an ex-regulator's analysis of what seems to be going on.

TW is a classic monopoly (apart from when it supplies business consumers). It has guaranteed revenues and zero competition. Its regulator is legally required to set its prices so that it can cover its 'efficient' costs and make a reasonable profit for its shareholders. It would take an impressive amount of mismanagement for it to lose money.

TW's prices and environmental performance are specified, in advance, in a licence to operate that lasts five years. Its current licence doesn't expire until April next year so it is far too soon for its shareholders to declare the company "uninvestable".

But there are some complications. Let's look at each of them.

Water Leakage and Sewage Discharges

No-one ever buys a product or service just because it is inexpensive. At the very least, we expect that it will be delivered to us within a reasonable time, and will not harm us. In regulators' jargon, we endeavour to maximise PQRS - an appropriate combination of the price that we are charged (P), the quality of the goods etc. being sold (Q), the range of products and services made available (R), and the associated service that is offered to customers (S).

In an unregulated market, we choose the combination of P, Q, R and S that best suits us at a particular time. We sometimes choose to shop in a large supermarket, and we sometimes pop into our local store. We sometimes shop in Harrods Food Hall, and sometimes in Lidl. We sometimes have an expensive meal in a posh restaurant, and sometimes we drive through a McDonald's.

This fundamental fact poses real problems for those involved in utility regulation. Put positively someone has to decide what quality, range and level of services should be provided, and at what price. Put negatively, it is no use forcing prices down if the regulated company is then allowed to provide a poor service to its customers.

This is a particularly important issue for, amongst others, the water regulator Ofwat which has the unenviable task of requiring water companies, such as Thames Water, to spend £ Billions to reduce water leaks and sewage discharges - with huge consequences for water bills. Luckily for Ofwat, most if not all of their environmental targets are set by the government and/or the Environment Agency. Ofwat are left with the task of calculating the cost to be passed on to customers.

But ... it certainly looks as though the water industry in general, and TW in particular, did not feel under enough pressure to reduce leaks or discharges. There may have been a number of reasons for this.

The UK's approach to price controls contains two perverse incentives.

First, as John Kay has pointed out, many - and sometimes most - people who work in utility companies are employed to stop things going wrong or to fix them when they go wrong. If most of those employees are sacked then water and electricity will continue flowing whilst costs fall and share prices rise, along with executive remuneration. And no attempt might be made to change course - until customers were poisoned or there was an extended failure of supply.

Others, including Dieter Helm, point out that price controls can encourage companies to neglect their capital assets such as pipework and sewage processing. "To win the efficiency competition [and so increase profits] you cut short-term costs sharply and that's what they did After more than 30 years all the consequences of those past decisions are showing up in the state of the assets now."

Then there is the point that Ofwat seems to have had inadequate powers. Having first issued licences many years ago, Ofwat could not legally change them (i.e. clarify and toughen them) without the approval of every company in the sector. The Government did not see fit to abolish this stupid rule until 2022.

The Current Discussions

TW and Ofwat have to agree (or the CMA on appeal has to impose) a PQRS settlement that will last until 2030. There is clearly no 'right answer'. Their task is made easier by the highly predictable nature of utility businesses. But there obviously remains lots of room for argument between company and regulator.

In the case of TW, Ofwat needs to decide how fast the company might be expected to reduce its (very high) leakage and its (also very high) sewage discharges into rivers, including the Thames - and how much these improvements will cost. The regulator needs to be realistic. No company can be expected to eliminate leakage and discharges overnight. But need this process take decades?

Also, to what extent should TW be allowed to charge for meeting leakage and discharge targets that it failed to meet in the current price control period?

The key point is that the best regulators adopt a realistic, firm but fair approach. Ofwat are hopefully doing this right now with a view to Ofwat's 2025-30 price determination being published next year. TW can appeal to the Competition and Markets Authority (CMA) if it thinks that the regulator has got it wrong. It is far too soon for TW's shareholders to be pressing the panic button.

TW's team is led by the well-respected Cathryn Ross who is a former boss of Ofwat. She is tough but sensible and there is therefore no reason to suspect that Ofwat's decisions will be stupidly tough, nor ridiculously weak. But I suspect that TW's customers will feel that Ofwat are (yet again?) being given far too long and allowed to spend far too much money to correct problems that should have been tackled years ago.

So why all the fuss?

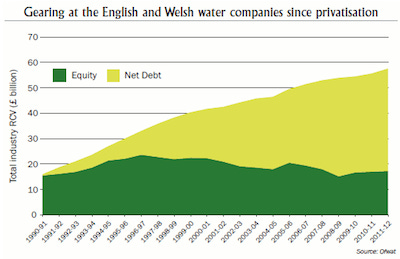

Companies raise money by issuing shares and borrowing money. Sensible companies do not borrow too much as a proportion of their share capital. Less sensible companies issue too few shares and borrow too much. TW were not sensible, in part encouraged by the tax system and low interest rates. They borrowed £18.3 billion and also interposed at least seven layers of companies between TW and its shareholders. They were not alone in doing this:

TW's debtors and shareholders changed over the years but now include various overseas sovereign wealth funds as well as pension funds, including the UK Universities Superannuation Scheme. They all employ well paid executives and advisers who were presumed to know what risks they were taking. I myself drew attention to the risks at least seven, and possibly more years ago. This web page containing this comment was archived in 2017:

" ...do investors realise how risky the shares are? It is possible, for instance, that the majority of investors are insufficiently focussed on the risk of a tough price control plus licence conditions which require substantial capital investment. A tough price control may well sharply reduce companies' profits, so sharply reducing their share prices (does anyone care?) or even forcing them into insolvency - in which case more would certainly care."

Those risks have now materialised as interest rates have risen, so the shareholders might lose all their money, and the debtors might lose a good proportion of the amount that they loaned to TW. Rather than hide in shame, they are beginning to argue that Ofwat should reduce their losses by cutting them some slack in the next price control, including increasing water bills (more than would otherwise be necessary) and reducing environmental fines.

Ofwat apparently see no reason to do so. TW's shareholders' and debtors' problems are not caused by an over-tight price control. So the government is preparing (if necessary) to cut the debtors and shareholder adrift and acquire TW, debt-free, through what is known as a Special Administration. This would ensure that TW will continue to provide water and sewage services and comply with safety and environmental standards rather than go through a messy insolvency.

Special Administration would be a (re-)nationalisation but it shouldn't require taxpayer funding, nor should it be characterised as a rescue. I also do not see it as a failure of privatisation. One might cynically be rather grateful to the ill-advised lenders and investors who poured money into TW only to lose much of it.

(There have been some highly technical press reports blaming the use by both regulators and investors of the Capital Asset Pricing Model (CAPM) to estimate what TW is worth and what needs to spend (by way of capital and interest payments) to finance its business. Criticisms of the CAPM are perfectly justified. I remember attending a presentation about its flaws around 20 years ago. But they do not excuse the ridiculous amount of financial engineering used by TW's shareholders over many years.)

But ...

Ofwat may have blundered in recent years by taking too great an interest in water company's governance, financing etc. Its Chair complained about the industry's corporate governance and low tax payments as long ago as 2013. Then, in 2018, the regulator announced strong incentives for water companies to reduce their dependence on debt financing. This didn't sound unreasonable but I became more concerned when the FT reported (13 April) that, as recently as 11 March, the regulator had written to the company demanding a reduction in group debt and that the company should investigate (a) a stock market listing and (b) breaking up the utility.

Most economic regulators try not to gets involved in company decision-making outside of PQRS because they then have to take responsibility if the alternative turns out to have unintended and undesirable consequences. TW's shareholders' response to Ofwat's letter may have been one of such consequences.

Further Reading etc.

Tim Leunig agrees with me that the government should not press Ofwat to propose a lenient price control:- What to do about Thames Water: Nothing!

Oliver Shah also agrees:- "If Thames Water's wipeout helps curb rentier capitalism, then good!" - Sunday Times Business Section 31 March 2024

As does Chris Giles - Financial Times 13 April 2024: "These issues are simple in capitalism. Owners and managers got things wrong. They deserve to pay the price for these fully-known risks that Thames agreed to bear when it accepted the latest licence conditions in 2019."

You can read more about water industry regulation here.

And please follow this link if you would like to read a longer introduction to the strengths and weaknesses of price controls.

(The Banx cartoon first appeared in the FT.)

Martin Stanley

Excellent overview and critique of how the current situation arose. Maybe Martin could expand it by adding an overview of how the water supply sector works in comparable countries - my understanding is that England is an outlier in the 'purity' of our privatisation model.